💳 Purchase & Financing Options

7 min

Think of solar financing like buying and financing a car with the added benefit of solar panels saving you money on your energy bills now and in the future.

There are 4 ways to go solar: you can buy your solar system outright, secure a loan to pay for it, choose a leasing program, or secure a power purchasing agreement. Whichever option you choose, solar panels can lower your price for home energy and put more money back in your pocket. Here's how they compare:

Cash Purchase

Homeowners with higher taxes often pay for their solar all up front and have the greatest return-on-investment over the lifetime of the system. With a cash buy the homeowner can claim all tax credits and rebates, avoid financing charges, and directly benefit from the savings on their electric bills. We have customers that have essentially no electric bills from the day they install solar.

In return for their upfront investment in a solar installation, homeowners will benefit from a reduced monthly electricity bill. For instance, let's say a solar system costs them $10,000 after all incentives and saves them $1,500 per year on their electric bill. To calculate the simple payback period — the approximate time for them to earn their initial investment back — we divide the cost of the PV system by the savings.

Simple Payback Period

$10,000 (System Cost) / $1,500/year (Annual Savings) = 6.7 years

The payback period for this system that costs $10,000 and reduces the electricity bill by $1,500 per year is 6.7 years.This doesn’t account for utility rate increases which would reduce the payback period as the savings per year would be increasing.

A solar system can last much longer than the duration of its payback period. In fact a typical rooftop solar system has a lifetime of about 35 years and has a warranty for 25 years. This makes the Solar Cash option the lowest-cost way to maximize their total lifetime savings.

Solar Loans

There are many, many solar loan options available today with various term lengths, rates, and structures.

Plenty of financiers offer $0 down loan options where the customer does not have to pay anything out of pocket to secure the loan and pay for the solar system. Most allow them to finance the full cost of their solar panel system with simple fixed monthly payments.

Many different types of institutions offer solar loans, from traditional banks to utility companies. Solar loans have the same basic structure, terms and conditions as other home improvement loans. Solar loans offer immediate returns by saving them money on their monthly electricity bills right away even as they repay the loan monthly.

Have you ever taken out a loan for a home renovation project? Solar panel loans are similar to home improvement loans that homeowners have used for decades to build a deck, upgrade their HVAC system, or add a second bathroom to their homes. And like these other types of loans, when they borrow money from a lender to finance a solar panel system they agree to pay it back plus interest in monthly installments over a set loan term.

The critical difference between a solar loan compared to a traditional home loan is how the Federal Investment Tax credit is factored into the payments.

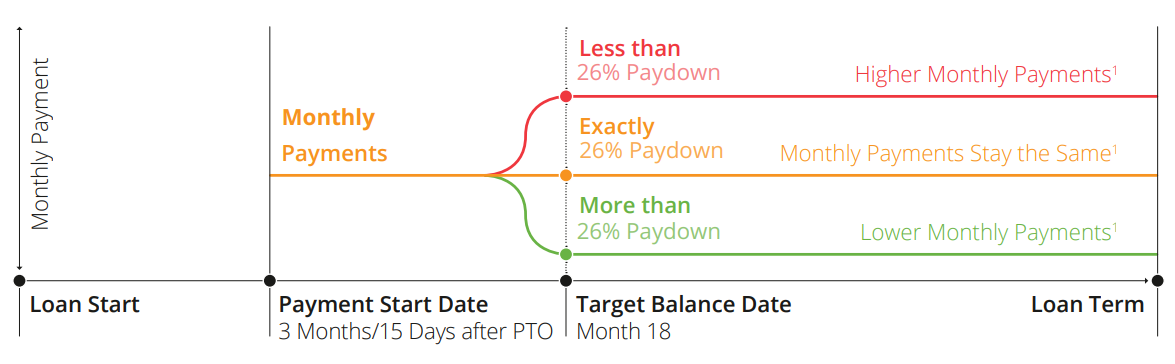

Here is an example of a loan for a $30,000 system:

The homeowner is eligible for a 30% ITC rebate equalling $10,000. The amount of the loan is $30,000 so the net cost for the customer is $30,000 - $10,000 = $20,000. This net cost of $20,000 is divided into monthly loan payments. The loan will stay configured like this for the first 18 months.

Even though the customer spends the first 18 months repaying the NET cost of $20,000, they still owe $30,000 gross for the system. The $10,000 credited to them from the Federal government makes up the difference between the gross and net amounts. Once the homeowner receives this payment they can keep it or pay it onto the loan.

The most common decision by customers is applying their Tax Credit of $10,000 to the loan as a “prepayment”. This keeps the total amount of the loan at the NET amount of $20,000 and thus monthly payments stay the same for the remainder of the loan.

However, should they choose to pay more than $10,000 down by month 18 then their monthly payments would reduce at month 19 until the end of the loan period. Conversely if they could not get the tax credit or decided to keep that tax credit money then their payments would increase as they were lent the full $30,000.

This structure of loan provides flexibility to the homeowner to choose how they want to handle their tax credit without having to pay interest and a higher monthly payment for the full system price.

Solar Lease

Solar leases are similar to car leases in that they are a form of third party ownership (TPO). Under a solar lease this third party owner (e.g. solar company) installs solar panels on a homeowner’s property and then rents them the panels which will produce a guaranteed amount of energy at a predetermined monthly rate. Companies calculate this rate based on the estimated annual production of their solar system and include this rate in their contract. A lease will also have a fixed term length which will typically range from 20 to 25 years. At the end of term a homeowner can generally choose to either purchase their system outright at the market value price, remove their solar system at no cost, or renew their contract (typically one to 5 years) and continue monthly payments.

Another important element in a solar lease is an annual escalator; these are becoming less common, but if included, will increase your monthly payment by a preset rate over your term length (typically one to five percent each year).

Under a solar lease, you won't own the solar system, but you will benefit from the electricity it generates.

You typically save 10 to 30 percent on electricity costs with a solar lease.

Solar Power Purchase Agreement

Financing a solar panel system with a power purchase agreement, otherwise known as a PPA, is similar to leasing or “renting” a solar panel system. Simply put, a solar company or PPA financier covers all the costs to buy solar equipment and install it on their roof. Though the solar panel system is located on their property the solar company owns it and therefore takes care of any necessary maintenance.

The solar panels generate electricity and power their home enabling homeowners to save on their monthly utility bills. In exchange they agree to pay the owner of the system (i.e. the PPA financier or solar company) a set rate for each kilowatt-hour (kWh) the solar panel system generates. In other words, they agree to purchase the power of the solar panels, hence the name PPA. This rate is typically lower than what their utility company charges for the electricity they would otherwise use from the grid.

Unlike with solar leases, PPA charges could vary from month to month since their bill is based on the production of the solar panel system. Because solar panels typically produce more electricity during the summer than during the winter, some people experience higher PPA payments during the summer months, but more savings on utility bills as well. There are balanced budget plans which provide a level payment plan similar to a lease with some providers.

Importantly, the majority of residential solar PPAs are $0-down. Some companies offer prepaid PPA options if they are interested in paying the entirety of the PPA upfront, but this is less common.

Yearly “escalators” in the PPA rate are also common but losing popularity.